Everyone knows that when you apply for a mortgage, the first thing lenders do is run your credit report. They look for great credit scores to qualify you for a loan. But what if you don’t have a credit score?

Does this exclude you from ever getting a mortgage?

The short answer is no, you can still get a mortgage. The more complicated answer though is that it depends on many factors.

Here’s how it works.

Why Lenders Care about your Credit History

Lenders use your credit history as a shortcut to determine if you are a good risk for a mortgage. In other words, it tells them are you likely or unlikely to pay your mortgage back on time? Lenders can tell in a matter of minutes what type of borrower and risk you are just by looking at your credit history.

Obviously, lenders only want to lend to people who will pay their mortgage back on time and a credit score makes that easy to determine.

To offer a loan with bad credit is a risk for lenders. Each lender has a minimum credit score threshold they prefer and if your score falls below it, you don’t qualify.

Is No Credit and Bad Credit the Same Thing?

Here’s the thing, though.

No credit and bad credit aren’t the same thing. They sound similar because neither offers lenders a ‘good feeling’ when they look at your application. However, no credit means you either pay cash for everything or you just haven’t borrowed money yet.

It’s most common for young adults just starting in life and retirees who have paid everything off and don’t have any real credit.

No credit doesn’t mean you are irresponsible. In fact, it might even mean you are exceptionally responsible and have paid for everything in cash.

Learn more: What Credit Score Do You Need to Buy a House

How to Get Approved for a Mortgage with no Credit History

So how do you get approved if you have no credit history? Every lender differs, but here are a few ways to make it happen.

Manual Underwriting

Today most lenders use automated underwriting. In other words, they put your information into a software program that uses an algorithm to decide if you should be approved for a mortgage.

It’s a bit cut and dry, which means if you’re qualifying factors don’t meet the requirements, you’re automatically declined. This doesn’t help borrowers who don’t have credit.

On the other hand, lenders that use manual underwriting don’t use a computer to underwrite the loan. Instead, they evaluate your application and qualifying factors manually (aka a human evaluates it) and can decide if you are a good risk.

Large Down Payment

In addition to finding a lender that uses manual underwriting, it doesn’t hurt to make a larger down payment than the minimum required.

For example, conventional loans require a 3% down payment for first-time buyers and 5% for subsequent homebuyers. But if you don’t have a credit score, lenders would be much more likely to approve your loan if you put down 20%.

The same is true of government-backed loans, such as FHA loans. While they only require a 580-credit score, it’s still a credit score. With no credit, you’ll want to put more money down than the minimum 3.5% down payment they require.

Low Debt-to-Income Ratio

Just as a larger down payment is helpful, so is a low debt-to-income ratio. With automated underwriting, some borrowers can get away with DTIs of 50% or higher.

When you don’t have a credit score to show your ability to repay a loan, though, lenders prefer a lower debt-to-income ratio. Ideally, your DTI would be no higher than 36%. This means your debts, including your new mortgage, shouldn’t take up more than 36% of your gross monthly income.

Consider a Cosigner

If you don’t have a credit score, and you only have the minimum down payment or you have a higher-than-normal debt-to-income ratio, a cosigner could be the key to getting your loan approved.

A cosigner with good credit shows lenders that there is someone else they can hold accountable for the loan, not just a borrower with no credit history. It helps if the cosigner also has a low debt ratio.

Learn more: 800 Credit Score Mortgage Rate

Compensating Factors when you Have No Credit

Lenders like it when you ‘make up’ for the fact that you have no credit.

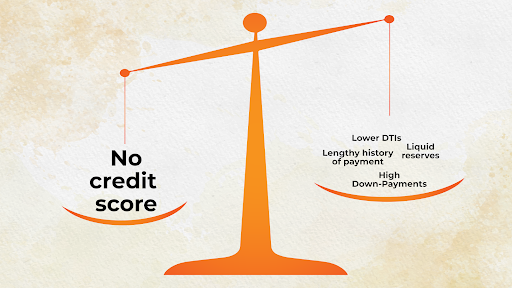

Ideally, you’ll have compensating factors that make up for the lack of a credit score. In other words, you have other factors that make your loan less risky, giving lenders a reason to approve your loan.

We already talked about higher down payments and lower DTIs, but other factors include:

A lengthy history of rent payments or other housing payments, such as paying cash for a house, but with a history of paying the real estate taxes on time.

Have ‘extra money’ available. Lenders call liquid money you have available that you don’t use for the down payment or closing costs ‘reserves.’ They calculate your reserves based on the number of mortgage payments it would cover. The more liquid reserves you have, the lower the risk of default you are.

Final Thoughts – How a Mortgage Broker can Help you Get a Mortgage with no Credit

You can get a mortgage with no credit, but you must prove beyond a reasonable doubt that you aren’t a risk of default.

Since most lenders require a credit score, you’ll have to look high and low to find a reputable lender willing to help you. When you work with a reputable mortgage broker, though, the job is much easier.

You’ll have someone working on your behalf to find a suitable lender within their network to help you get a loan without any credit. Again, this doesn’t mean you need a loan with bad credit, but instead, you need a loan without any credit history because you’ve either paid cash for everything, paid all your loans off, or you are just starting out in life and haven’t built up a credit score yet.