Dealing with bankruptcy is tough, there's no way around it. Beyond the immediate stress, it often casts a long shadow, making big dreams like owning a home feel distant or even impossible. Many people understandably worry that they've lost their chance at getting a mortgage, or at least one with decent interest rates, for a very long time.

But here's some good news, especially if you're reading this, because that worry doesn't have to be the end of the story. People absolutely do successfully buy homes after bankruptcy, and they often secure surprisingly good mortgage rates. It takes time, effort, and a clear plan, but getting the keys to a new home is definitely achievable. Let's walk through how others have navigated this path successfully.

1. The First Step: Patience and Planning (The Waiting Period)

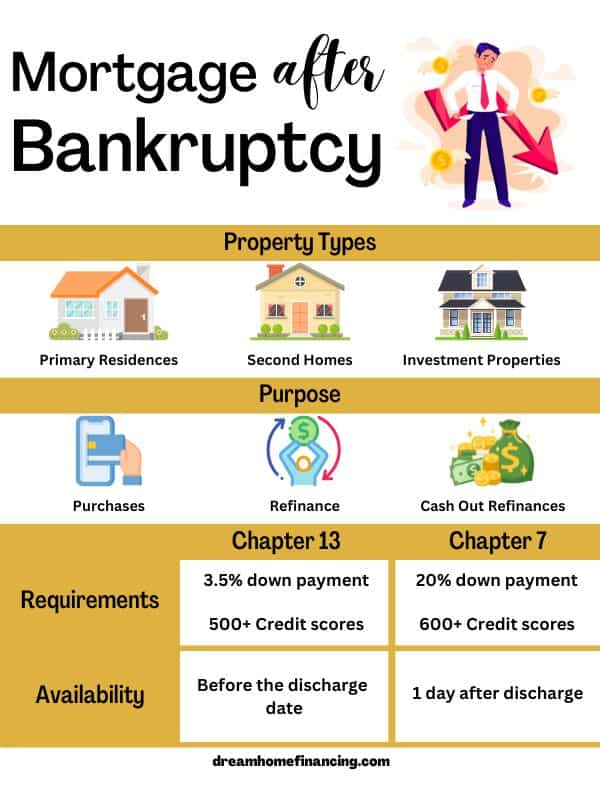

Okay, first things first: you can't jump straight from a bankruptcy discharge into a mortgage application. Lenders need to see that some time has passed and that your financial footing is getting stronger. This is often called the "waiting period." How long you generally need to wait depends on the type of bankruptcy and the kind of mortgage you're aiming for:

- FHA Loans: Often require about 2 years after a Chapter 7 discharge. With Chapter 13, it might be possible after 1 year of making plan payments on time (with court permission) or sooner after discharge than with Chapter 7.

- VA Loans: Similar to FHA, usually looking for about 2 years after Chapter 7, or sometimes 1 year of solid payments in Chapter 13.

- USDA Loans: Typically need about 3 years after Chapter 7, potentially less time after a Chapter 13 depending on payment history.

- Conventional Loans: These often have the longest waits, frequently 4 years after Chapter 7 (though sometimes less if there were specific, documented hardships) or maybe 2 years after a Chapter 13 discharge.

(Quick reminder: These are common timeframes, but lending rules can shift. It's always smart to check the latest guidelines when you're getting closer to applying!)

Think of this waiting time not just as waiting, but as active preparation time. It's your chance to rebuild and get ready.

2. Rolling Up Your Sleeves: Rebuilding Your Credit

Bankruptcy takes a heavy toll on credit scores, and lenders look closely at those scores. A lower score signals higher risk, which can mean higher interest rates. So, focusing on rebuilding credit is absolutely essential. People find success by:

- Keeping a Close Eye on Credit Reports: Getting free copies of reports from Equifax, Experian, and TransUnion (check AnnualCreditReport.com) is step one. People look them over carefully to make sure the bankruptcy details are right and spot any errors that could be dragging their score down.

- Building New Positive Credit History: It might sound odd, but lenders need to see that you can handle credit responsibly now. Some good tools for this are:

- Secured Credit Cards: You put down a deposit, and that's usually your credit limit. Using it for small things (like gas or a streaming bill) and paying it off in full every month shows responsible use.

- Credit-Builder Loans: Some credit unions offer these. They're small loans designed specifically to help people build or rebuild credit through on-time payments.

- Making On-Time Payments Non-Negotiable: This is huge. Paying everything on time – rent, utilities, any car payments, and especially those new credit-building accounts – is the biggest factor in boosting a credit score. Consistency is king.

- Using Credit Wisely: Keeping balances low on credit cards (even if paid off monthly) helps scores. Aiming to use less than 30% (and ideally less than 10%) of the available credit limit is a good goal.

- Hitting Pause on Other New Debt: Aside from the tools used specifically for rebuilding, successful borrowers usually avoid taking on other significant new debts during this recovery phase.

3. Building a Safety Net: The Power of Saving

While working on credit, saving money is the other key piece of the puzzle. Yes, you need funds for a down payment and closing costs. But saving consistently also sends a powerful message to lenders: the past financial troubles are truly in the past, and you're now managing money reliably. Even saving small amounts regularly adds up and shows discipline and stability – important qualities for any homeowner.

4. Finding the Right Partner: Lenders and Preparation

Not every bank or lender is the right fit for someone recovering from bankruptcy. Some are simply more experienced or comfortable with these situations than others.

- Shopping Around is Key: Don't just walk into the first bank you see. It pays to research lenders, talk to mortgage brokers (who work with multiple lenders), and look for those who frequently handle FHA, VA, or loans for people rebuilding credit.

- Being Open and Honest: It's best to be upfront about the bankruptcy. Lenders will see it on the credit report anyway, so honesty builds trust right from the start.

- Getting Your Paperwork Ducks in a Row: Lenders will ask for more documents after a bankruptcy. Being prepared makes things smoother. Gather things like:

- Bankruptcy discharge papers.

- Recent pay stubs, W2s, and tax returns.

- Bank statements (to show savings and responsible spending).

- A Letter of Explanation (LOX): This is your chance to briefly explain, in your own words, what led to the bankruptcy, what you learned, and how things are different now. Taking responsibility, not making excuses, goes a long way.

5. The Home Stretch: The Application Process

When it's time to apply, expect the lender to take a very close look at everything – income, credit, savings, job stability. It might feel like being under a microscope, but it's standard procedure as they need extra assurance. If you've spent the waiting period rebuilding credit, saving diligently, and have all your documents ready, this part, while detailed, becomes much more manageable.

Crossing the Finish Line: Success IS Possible!

Getting that mortgage approval, especially with a good interest rate, is a huge relief and a major win. It’s proof that the hard work and discipline paid off. Achieving a competitive rate usually happens because:

- Enough time has passed since the bankruptcy.

- The credit score has clearly recovered thanks to consistent effort.

- There's solid proof of savings.

- Income is stable.

- The borrower found a lender who understood their situation.

Your Path Forward: Encouragement and Key Takeaways

If you're on this journey toward homeownership after bankruptcy, don't lose heart. It takes time and focus, but countless people have successfully done it.

- Use the waiting period to actively rebuild.

- Make credit repair a top priority.

- Save consistently – every bit helps build confidence and stability.

- Be prepared and honest when talking to lenders.

- Don't be afraid to shop around to find the right lending partner.

Bankruptcy doesn't have to be a life sentence excluding you from owning a home. Think of it as a detour. By taking things step by step and focusing on rebuilding, getting those keys to your own place, with a mortgage rate you can feel good about, is absolutely within reach.

Keeping track of your credit repair journey??? Get the checklistHERE

Disclaimer: This information is intended to be encouraging and informative, based on common experiences and general lending practices. It's not personalized financial or legal advice. Mortgage rules, loan programs, and credit scoring change over time. Always talk with qualified mortgage professionals and financial advisors to figure out the best approach for your unique situation.